Compared to returns from exploitation, returns from exploration are systematically less certain, more remote in time, and organizationally more distant from the locus of action and adaption.

James G. March, Exploration and Exploitation in Organizational Learning (1991)

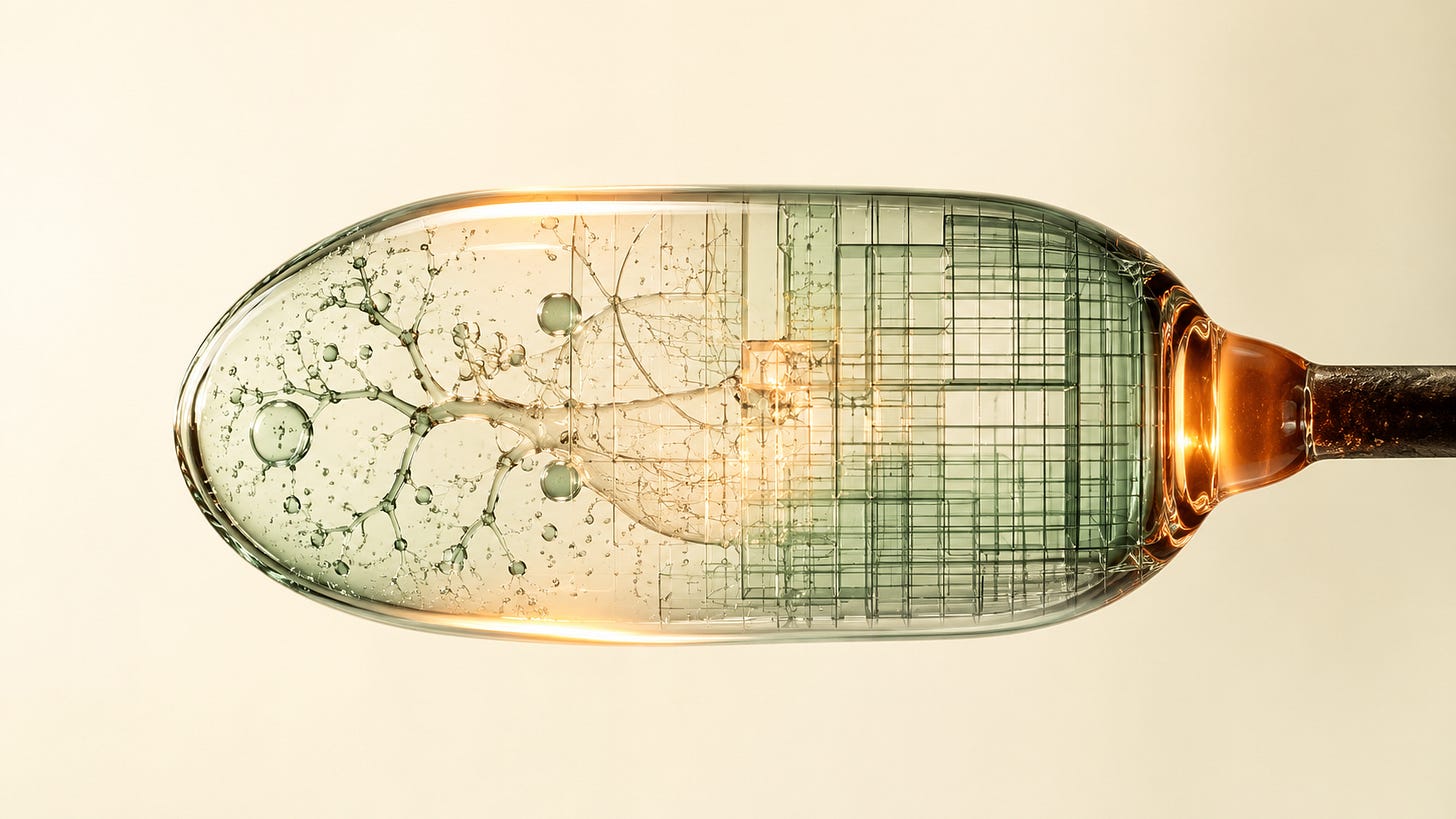

Product-market fit. It’s that beautiful moment every startup strives for. The moment that you realise you have made something people really want. And it’s usually at that moment that something quietly loud happens. A company is pushed to go from exploration to optimisation. Consistent returns demand it. The warm glass needs to set.

When there’s a consistent revenue source, the company can begin to really scale, push on marketing, sales, operations, etc. Double down on the winning horse, so to speak. This is the point at which the CFOs I used to consult for would start to take less aspirin. After all, risk is for startups, a proper company needs to grow up. One CFO of a global logistics company once told me: “Oh, we never want to be a pioneer in our industry, always a fast follower.” Later, on the way home I saw an advert of their’s that stated something to the like of, “Leading the way with technology since…”

James Kerr - The Wayfinder Notes is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

The truth is that this outlook is very common, for good reason. I already talked about it in The Icarus Intelligence Problem: pioneers absorb the force, fast followers ride the slipstream. And when a big firm did want exploration on the books, it kept it at arm’s length: an R&D department slightly off to one side, its own budget, its own clocks, a protected annex bolted onto the optimising machine. March’s line above is why the wall existed. Returns from exploring arrive later, less certainly, and further from home, so wherever the two share a desk, the machine wins the argument every week.

However, all of this rests on one assumption: the thing you’re optimising for stays long enough for people to pay you enough for it.

Hungry Birds

This morning I opened two apps I love and use every day, Granola and Littlebird, and found something funny. I pressed on Littlebird’s new meeting-notes update and found a Granola clone, redrawn (screenshot below; not the only company following Granola, but one of the more brazen, design-wise). Nobody involved did anything unusual or unexpected. Maybe it’s poor taste to be so on the money but copying a working product is now so cheap and so quick that it’s simply part of what shipping looks like.

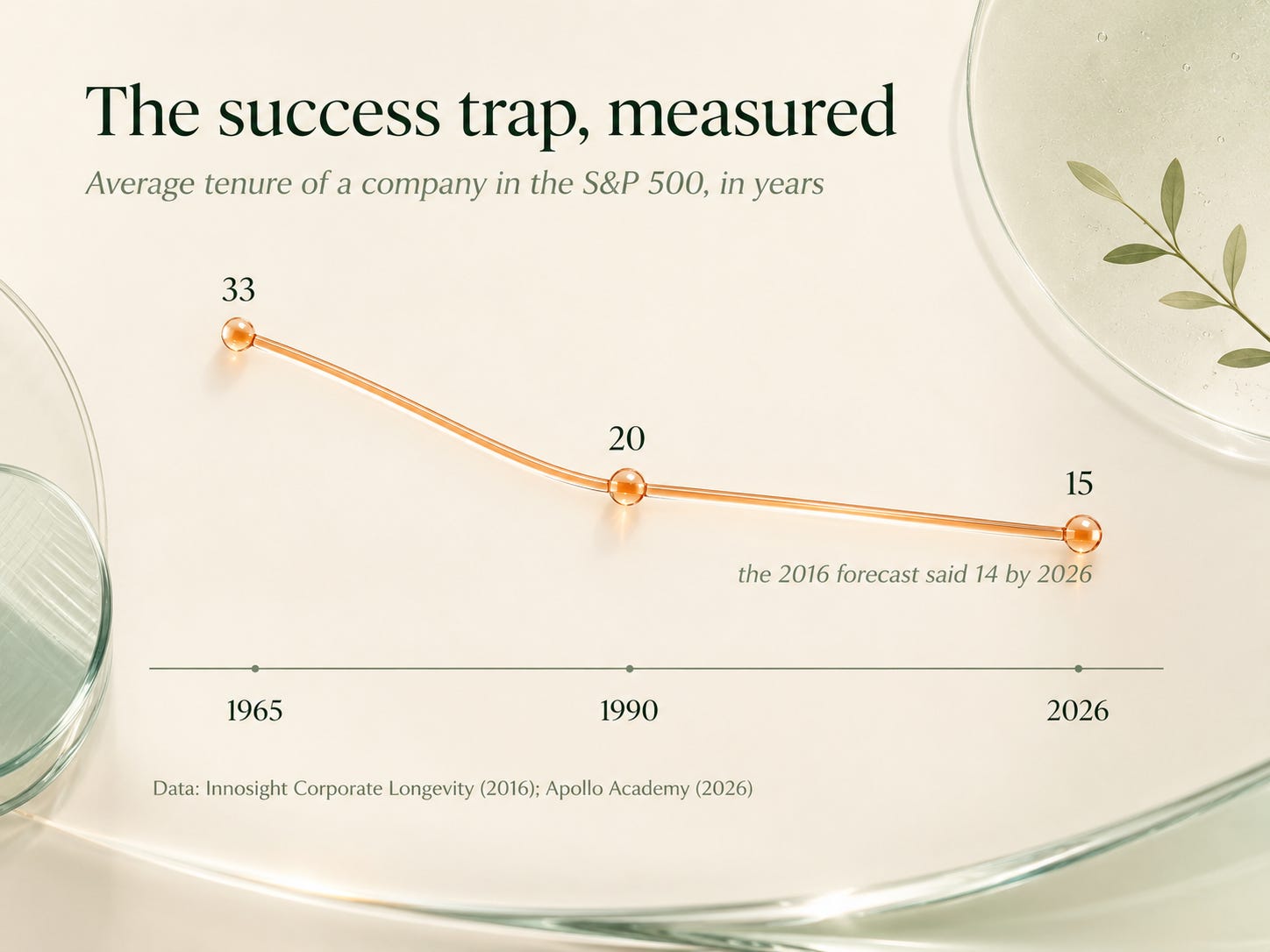

So I did some other research with [insert one of many AI research tools] (I kid, but also so I don’t seem like I’m doing unpaid product placement) and found another accelerating trend of interest to this: in 1965 the average company on the S&P 500 had held its place for 33 years ; by 1990 it was 20; today it's about 15. An MBA would call this ‘sustained competitive advantage’: how long a company on average can keep their competitive edge and make revenue from it.

In A Promethean Pickle I wrote that building in public gives the game away; the update is that building in private only buys a few weeks now, because whatever the market can see shipped, it can see cloned.

So the glass never gets to set. Optimise-only puts all your eggs in a few very obvious baskets; explore-only never compounds your gains on the thing that will give you returns; what’s left is an increasing need for young companies to be in both modes at once, permanently. Call it the teenage company: old enough to have something that works, young enough to still be working out what it’s going to be. Adolescence is the one awkward stretch where being and becoming run at the same time... and companies need to try to find it repeatedly in adjacent fields until they find their safe moat.

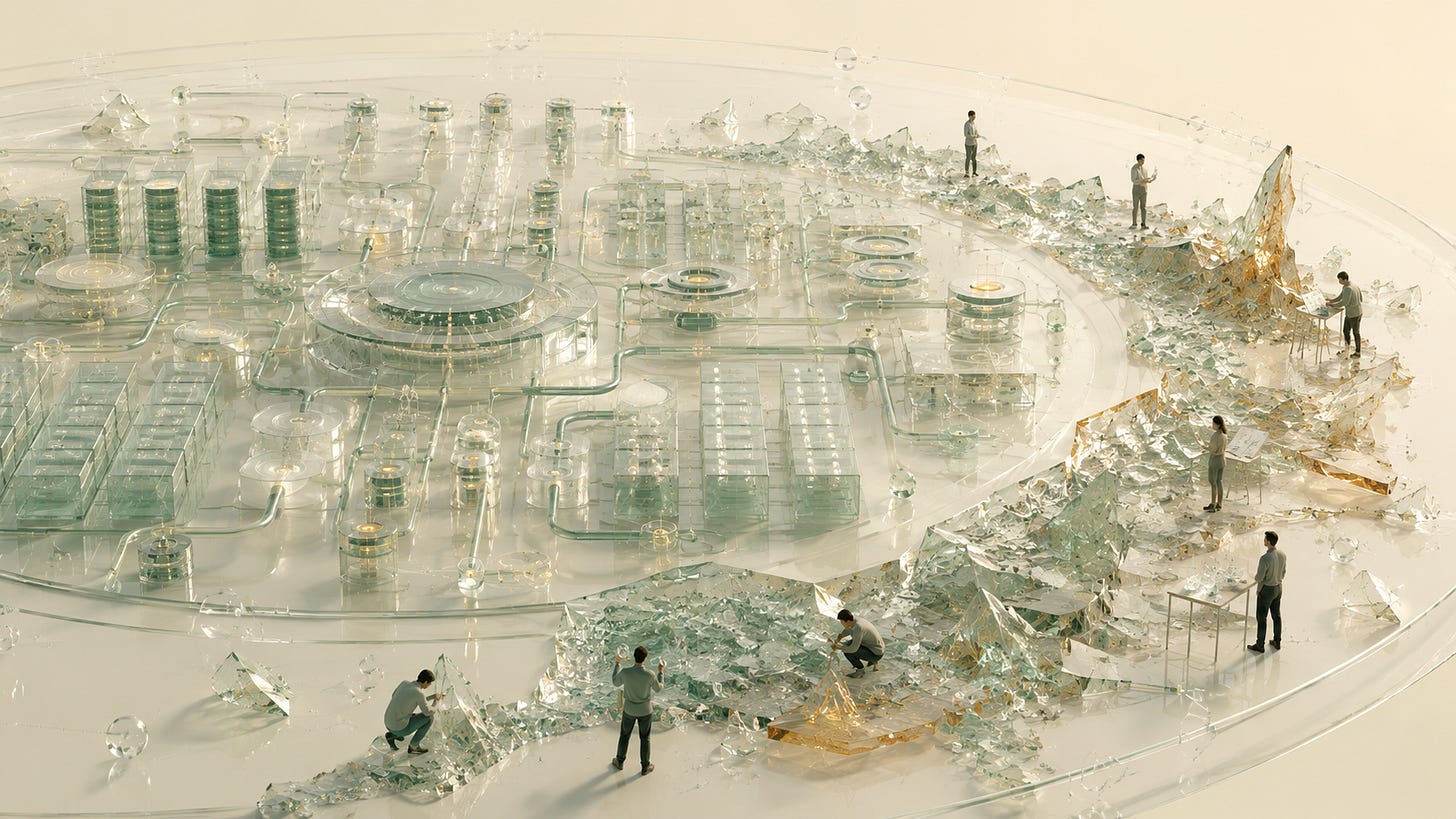

Systems for Scale

The companies of the future need to set their operating models to look for growth AND optimisation at the same time , but ensuring that it bleeds into every part of company culture. They could afford it: a money printer funded a professional exploration department (the R&D dept.), which is why "be more like Amazon" was never much use to a twelve-person firm. What capital bought was the freedom to experiment and innovate mostly in isolation from the core business model. That luxury, as we’ve just explored, is ceding fast. The captured, repeatable side of a business (the reporting, the pipeline, the playbooks) can now run substantially on agents, so the human hours go back to the frontier since a failed experiment costs an afternoon rather than a quarter.

Experimentation now needs to be ingrained in company culture at the ‘Jagged Edge’ of Agent Intelligence

Whether you're a bootstrapped solopreneur or a VC-backed small to medium-sized enterprise, a marketing agency even... the key here is in setting up systems for scale . Consistently set up systems that can monitor competitor events. Then turn your attention to optimising for customer service on the product lines that work. Always try new things in your marketing in order to test where demand is and how it is shifting in the market, consumer tastes may change under your feet. Keep the trying boringly small (one experiment at a time, decided by Friday), choose key metrics and thresholds beforehand, write the survivors into playbooks the machines hold, and put every candidate through the one qualifying question: if this worked, would we double down?

In the coming weeks, I’ll go into exactly what this looks like for a small advisory and platform start-up like our’s at CURN and offer a few assets to help.

In the meantime, keep well.

James Kerr - The Wayfinder Notes is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.